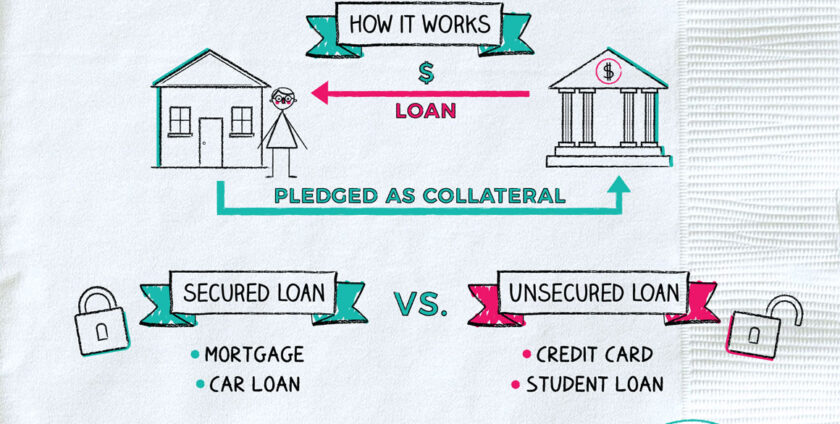

If you don’t have the best credit and want to lock in a low interest rate or borrow a large amount of money, a collateral loan might be on your radar. Unlike unsecured personal loans, collateral loans require you to pledge an asset like a savings account or car, which the lender can take if you don’t repay the loan.

Let’s take a closer look at what collateral loans are, where you can get them, and some pros and cons to consider.

If you’re considering an unsecured personal loan, you can visit Credible to learn more and to see your prequalified rates.

How do they work?

Also known as a secured personal loan, a collateral loan is guaranteed by collateral, or something valuable you own. This might be a house, car, savings account, investment portfolio, or even a piece of jewelry or musical instrument. If you default on your loan, the lender will be able to seize your collateral. You can use a collateral loan for nearly any purpose, whether you need to cover an unexpected expense, pay a medical bill, or make an expensive car repair.